VNE S.p.A. lists on Euronext Growth Milan

Equity Trading - Summer 2023

As the summer period is approaching, we are glad to share a recap of the first half of 2023 with (1) evolution of market share across exchanges and MTFs, (2) the successful migration of Italian cash markets onto Optiq, as well as (3) the upcoming expansion of the Global Equity Market for pan-European and US stocks, and (4) the launch of dark trading and midpoint functionalities on Euronext Central Limit Order Book.

Highlights

Looking back...

- Continuous & auctions market share has improved for the main Regulated Exchanges on their respective ‘domestic shares’ in 2023, with Euronext increasing from 62.9% in January to 66.5% in June.

- The migration of Italian cash markets onto Optiq led to strong improvement of Euronext market quality as the venue for price formation, with Euronext Milan market share reaching the highest in 18 months – and EBBO Setting Percentage increasing from 50% to over 68%.

and looking ahead

- Euronext will expand its retail offering on the Global Equity Market (GEM) and Trading After Hours (TAH): over 300 pan-European and US shares will be available for trading from 07:30 to 20:30 CET, cleared and settled in Euros, with the same market microstructure and connectivity as Euronext main markets.

Euronext will launch dark, midpoint and dark-lit sweep functionalities on its Central Order Book by the end of 2023, at zero latency for dark-to-lit execution.

Market share increased for Regulated Exchanges in Europe

- All Primary Exchanges have gained market share from MTFs compared to the beginning of the year – both during the volatile Q1 and after the quiet Q2.

- Euronext has reached 66.5% market share - highest in the last 12 months.

*Continuous & Auctions market share on domestic stocks, including dark and periodic auctions.

Data source: IRESS Market Data

Euronext Milan market quality improved after Optiq migration

- Euronext reinforced its position as the venue of price formation following the migration of Italian cash equity markets to Optiq on 27 March 2023.

- Euronext Milan reached 73.8% market share in June 2023, the highest level over the last 18 months.

- Euronext EBBO Setting Percentage for FTSE MIB stocks increased from 50% in Q1 to 68% in Q2 – while each of the main MTFs now sets the best prices on Milan blue chips less than 15% of the time.

Data source: BMLL Technologies

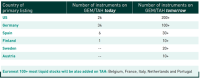

Pan-European and US stocks on Euronext GEM

- Euronext Global Equity Market (GEM) is an MTF managed by Euronext already offering already 100+ European and US blue-chip stocks, with more to be added soon.

- Trading After Hours available until 20:30 CET, overlapping with US markets.

- Same connectivity, microstructure and trading platform as Euronext main markets.

- 40+ members connected already: retail banks, global brokers and market makers.

- A full revamp of Euronext GEM will take place after the summer, with a dedicated market making scheme and an expanded stock universe.

What do I need to start the membership process on Euronext GEM?- A set-up with Euronext Clearing (CC&G) is required - But you can start the membership process/paperwork now - No membership fees - No additional market data fees - No additional Logical Access fees – same connectivity you already use for Euronext main markets |

Euronext will launch dark, midpoint and sweep functionalities

- The latency between Euronext and London MTFs has multiplied by ~10 since the migration of the Euronext Data Centre from Basildon (UK) to Bergamo (Italy), thus Dark to Lit execution performance is deteriorating on MTFs.

- Euronext will launch dark functionalities to source liquidity in both trading pools (Dark and Lit) within the Central Order Book – not a separate MTF.

- Thanks to sweep functionalities, orders can be transferred to the Euronext Lit Central Limit Order Book in case of partial or no execution in the dark – at no latency.

- Timeline: Q4-2023 in test environment and Q1-2024 in production.

Focus on Latency – How long does it take for an order sent from London to reach the Euronext Data Centre in Bergamo?From 0.5 milliseconds before the Data Centre moved from London to Bergamo in June 2022, to 3-4ms (microwave) or 7-8ms (fibre) today. Data source: big xyt - Euronext will close this gap offering Dark to Lit execution at no latency, within the same Central Limit Order Book and leveraging on the Data Centre in Bergamo. |

The Euronext Equities team

In the news

The TRADE News - 16 May 2023

Euronext to launch dark trading and expanded retail trading services amid second best quarterly results in its history

New dark offering is aimed at reducing latency arbitrage for clients following the exchange’s data centre migration, Euronext’s Simon Gallagher and Vincent Boquillon told The TRADE.

Read the article

At conferences in H2-2023

- International TraderForum,

5-8 September, Barcelona - FIX Trading France,

14 November, Paris

Check out our insights on LinkedIn in H1-2023

Click on the links below:

What should be addressed in MiFIR Review

The TRADE Roundtable: Trading at the Closing Auction

The Price of Liquidity in Equities' panel at FIX EMEA 2023

For more information

Don't hesitate to contact your sales representatives with any queries or feedback.

Thank you!

Riba Mundo Tecnología S.A. lists on Euronext Growth Milan

INTERBOLSA Fee Books update – January 1, 2019

Interbolsa amended its price list for Financial Intermediaries following the European Central Bank’s decision to increase prices charged for the settlement and account movement through the TARGET2-Securities platform, effective January 1, 2019.

In the strategy defined by Interbolsa, for the prices to be charged in 2019, it was decided to pass on its prices the cost increase with the T2S platform, updating the prices related to settlement and account movement.

Following the project of links between Interbolsa and other European CSDs, which allow cross-border transfers of debt securities between the participants of these CSDs and Interbolsa participants, the link between INTERBOLSA and Clearstream Banking AG (CBF) is in the test phase. Therefore, the prices to be charged for the maintenance of the securities registered in the CBF in the Interbolsa participants’ accounts have already been defined. The following changes were made to Financial Intermediaries’ Fee Books:

Addition of a new paragraph to point 5.1, defining the rules for the application of maintenance fees for debt securities registered in CBF;

Inclusion of Table 6 to point 5.1, establishing the annual percentages to be applied for the purpose of calculating the monthly maintenance fee.

With regard to the prices charged to Issuer Entities, Interbolsa’s Board of Directors decided to reduce the prices charged for the registration and cancellation of issues of warrants and certificates with the purpose of increasing the registration of this type of financial instrument in Interbolsa’s systems.

The fees applied to the manual corrections to the exercise of rights in process or already processed have been changed in order to reflect the risk assumed by Interbolsa.

Interbolsa decided to charge the costs of disclosure information to the market, requested by several entities (issuers entities, paying agents, law firms …). The points 8.7 and 6.10 was added in the price lists of Financial Intermediaries and of the Issuers Entities, respectively.

These amendements shall take effect on 1st of january 2019.

Amendment of Regulation 1/2016

RGPD application and repeal of INTERBOLSA circular 1/2001, relating to the Issuer Agent

In accordance with the legislation and regulations in force, INTERBOLSA provides to the issuers, with registered securities, the service related to the identification of securities holders.

As a service provided by law to the issuers, that request the service, the entities involved in the process of collecting, processing, storing and forwarding of personal data (such as shareholders, banks and INTERBOLSA) cannot refuse to provide this service or to provide the necessary information.

However, without prejudice to the above, and taking into account the application of the General Data Protection Regulation (GDPR), which entered into force on May 25, 2018, INTERBOLSA considered to be relevant to include in INTERBOLSA Regulation 1/2016 a specific provision concerning the protection of personal data in order to make transparent and reinforce the transmission to INTERBOLSA of the personal data collected by the financial intermediaries and the treatment of such data by INTERBOLSA in compliance with the applicable legal provisions.

In order to properly accommodate this change, INTERBOLSA added article 17-A to INTERBOLSA Regulation 1/2016, related to the Participants in the systems managed by INTERBOLSA.

The opportunity is also taken to eliminate article 1 (4) of INTERBOLSA Regulation 1/2016, as well as INTERBOLSA Circular 1/2001, related to the Issuer Agent.

Open Investment Funds registered at INTERBOLSA

INTEBOLSA offers a new functionality in the Investment Funds System – order routing, allowing Fund Managers to directly confirm/reject the operations of subscription/redemption.

This new feature allows also Custodian/ Settlement Entities to be able to monitor the entire subscription and redemption process, including the financial settlement, whenever it occurs in their cash accounts (DCA).

To properly accommodate this amendment, INTERBOLSA revoked INTERBOLSA Circular 1/2017 and replaced it by INTERBOLSA Circular 1/2019, as well as amended the INTERBOLSA Timetables Notice.

CSDR – Settlement Discipline Workshop

The Settlement Discipline regime is a key feature of the CSD Regulation (CSDR) which will introduce changes to CSDs throughout the European Economic Area and aim to promote their operational efficiency and thus contribute to a timely and efficient settlement in the European Union.

The CSDR – Settlement Discipline Workshop, which took place in Lisbon on 18/09/2019, is part of the preparatory work that INTERBOLSA has been developing with its Participants and the Market, with the aim of providing them with the essential tools for the entry into force of this new regime in September 2020.

The presentation made at the Workshop is available at the following link.

INTERBOLSA decreases the resubmission of instructions fee from 83 cents to 33 cents

INTERBOLSA has decided to amend its price list for Financial Intermediaries and other entities by reducing the resubmission of instructions fee from 83 cents to 33 cents from 1 October 2019.This fee will be charged to the parties involved in the transaction, per resubmission day, whenever an instruction not settled is resubmitted on the T2S platform for a new settlement.

Following the adoption of the Trade Date Netting (TDN) model by all the CCPs participants of Interbolsa, it has also decided to change the charge of the cancellation of instructions, beginning on October 1, 2019, this fee to be charged to all cancelled operations.

Non-euro Currency Settlement System

The Non-euro Currency Settlement System (SLME), managed by INTERBOLSA accepts, since September 30, 2019, the settlement and income payments related to Exchange-Trade Funds (ETFs) denominated in a non-euro currency.

The list of eligible currencies has also been extended to the:

- Chinese offshore;

- Norwegian krone;

- Swedish krona.

The Non-euro Currency Settlement System processes the settlement of all operations in non-euro eligible currency, namely the settlement of operations carried out over-the-counter, the settlement of “non-clearable” market operations and the income payments and redemptions.

To properly accommodate these amendments, INTERBOLSA amended the INTERBOLSA Regulation No. 2/2016, the INTERBOLSA Circular No. 1/2016 and the INTERBOLSA Circular No. 4/2016.

“Partial Release” functionality

INTERBOLSA has made available the “Partial Release” functionality with the implementation of the T2S Change Request 653 with Release 3.2, occurred on November 16, 2019.

This new functionality that introduces benefits in improving settlement efficiency, enabling fails reduction in accordance with the future CSDR settlement discipline regime, meets the following requirements:

- Available only for securities delivery instructions (DVP, DFP and DWP);

- For settlement instructions:

- matched and not canceled;

- pending with Party “Hold”;

- that permit partial settlement;

- which intended settlement date (ISD) has been reached.

In cases where the partial quantity released does not settle, during the day the partial release functionality was activated (until the end of the respective cut-off), the process will be automatically canceled by T2S, returning the instruction to its original status (Hold of initial quantity).

To properly accommodate this amendment, INTERBOLSA revised Article 46 of INTERBOLSA Regulation 2/2016 (amendment of paragraph 2 and addition of paragraph 4).

Supplementary documentation: Release 3.2 Briefing Paper